Yes, homeowners insurance, also called house insurance, covers fire damage, because fire is a core covered peril. A standard policy pays for the dwelling structure, your personal belongings, smoke and soot damage in rooms the flames never reached, the water used to extinguish the fire, and Additional Living Expenses while the home is repaired. The main exception is arson by the owner.

Homeowners Insurance and Fire Damage: What Is and Is Not Typically Covered

Most standard homeowners policies cover fire and smoke damage broadly, but a handful of exclusions can reduce or deny a claim if insurers determine the cause falls outside normal coverage.

| Typically Covered | Typically Not Covered |

|---|---|

| Structural damage to the dwelling from an accidental or electrical fire | Intentional fire set by the policyholder (arson) |

| Personal contents and belongings damaged or destroyed by fire or smoke | Damage to a home left vacant for an extended period, typically 30 to 60 or more days (varies by policy) |

| Smoke and soot damage to walls, ceilings, HVAC systems, and personal property | Damage attributed to neglected or uncertified electrical wiring the insurer can show the homeowner knew about |

| Water damage caused by firefighting efforts, including hose water and sprinkler discharge | Government-ordered demolition or clearing of property (may require separate coverage) |

| Additional living expenses (ALE) while the home is uninhabitable during covered repairs | High-value items (jewelry, art, collectibles) above per-item limits without a scheduled rider |

| Detached structures such as garages and fences, typically at a percentage of dwelling coverage | Business property or equipment stored at home beyond the personal property sublimit |

The Short Answer

Yes, a standard homeowners insurance policy covers fire damage. Fire is what the industry calls a core covered peril, which means it is one of the fundamental disasters your policy exists to protect against, right alongside things like windstorm and theft. If your home catches fire, whether from faulty wiring, a kitchen accident, a space heater, or a lightning strike, your policy is designed to help you rebuild.

That is the reassuring headline. The detail worth understanding is that a fire claim is rarely just about burned walls. A house fire creates several distinct kinds of damage at once, and a good policy is built to handle all of them together. Knowing what falls under your coverage keeps you from leaving money on the table when you need it most.

What a Fire Policy Actually Covers

When fire strikes a home, a standard policy generally steps in across four main areas:

- The dwelling structure. This is your home itself, the walls, roof, floors, and built-in systems. Fire coverage pays to repair or rebuild the physical structure that burned.

- Your personal property. The belongings inside, furniture, clothing, electronics, appliances, and the everyday things that make a house a home, are covered up to your policy limits when fire destroys or damages them.

- Smoke and soot damage. The residue and staining that fire leaves behind on surfaces and contents, even in rooms the flames never reached.

- Additional Living Expenses. If the home is unlivable while it is repaired, your policy helps cover the cost of staying somewhere else.

The theme is that a fire claim treats the event as a whole, not just the charred spots. That matters, because the damage a fire leaves behind spreads far past the room it started in.

💡 Fire Damage Is Rarely Just Fire

By the time a house fire is out, you are usually dealing with three problems layered on top of each other: what the flames burned, what the smoke and soot coated, and the water used to extinguish it. A standard policy is built to address all three under the same fire claim, which is exactly why a full restoration involves more than a contractor patching drywall.

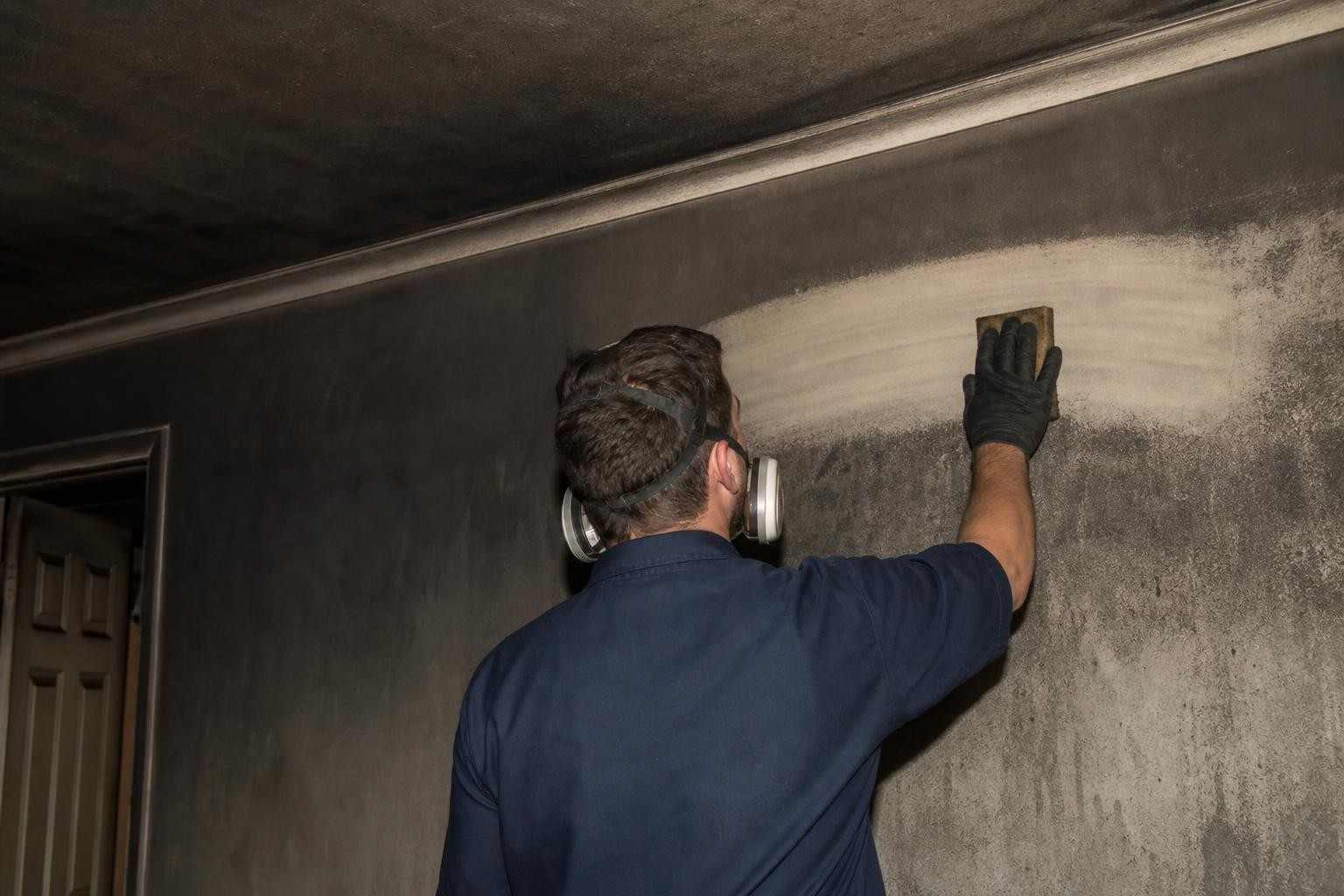

Smoke and Soot Damage Are Covered Too

One of the most misunderstood parts of a fire claim is smoke. Flames might be contained to a single room, but smoke and soot travel through the entire home, settling into walls, ceilings, ductwork, fabrics, and belongings far from the fire itself. That damage is real, and it is covered under the same fire peril as the flames.

Soot is acidic and corrosive, so it keeps damaging surfaces the longer it sits, etching glass and metal and staining porous materials permanently if it is not cleaned quickly. The smell alone can make a home unlivable. This is why proper smoke and soot damage cleanup is a specialized job and a legitimate, coverable part of your claim, not an optional extra you should try to skip to save the insurer money.

The Water Damage From Putting the Fire Out

Here is the part almost no one thinks about until they are standing in it. Firefighters use an enormous amount of water to put out a house fire, and that water soaks floors, walls, ceilings, and everything in between. The good news is that water damage caused by extinguishing a covered fire is itself covered under your fire claim. You do not need a separate flood or water endorsement for it, because the water is a direct result of the covered fire.

And that water does not just disappear when the fire is out. It sinks into drywall, subfloors, and framing, and if it is not extracted and dried properly within a day or two, it becomes a second disaster of its own: warping, structural damage, and mold. That is why fast water extraction is a critical early step after a fire, not an afterthought once the smoke clears.

⚠️ The Fire Is Out, but the Clock Is Not

Firefighting water left in the structure follows the same rules as any other water damage. Per EPA guidance, water-damaged areas should be dried within 24 to 48 hours to keep mold from taking hold. After a fire, that water is easy to overlook while you deal with the shock, but leaving it to sit turns one covered loss into two problems.

Additional Living Expenses: A Place to Stay

If a fire makes your home uninhabitable, you should not have to pay out of pocket to have a roof over your head while repairs happen. That is what Additional Living Expenses coverage, often shortened to ALE and sometimes called loss of use, is for. It helps pay for the reasonable extra costs of living away from home during the repair, such as a hotel or short-term rental, and in many cases meals and other necessary expenses above your normal spending.

ALE is one of the most valuable and most forgotten parts of a fire policy. A serious fire can leave you displaced for months, and those living costs add up fast. Keep every receipt from the moment you are displaced, because that is what you submit to be reimbursed. Ask your adjuster early what your ALE limit is and what it covers, so you are not guessing while you are already under stress.

When a Fire Is Not Covered

Fire coverage is broad, but it is not unconditional. There are a couple of honest exceptions worth knowing:

- Arson by the owner. If you intentionally set the fire yourself, or arrange for someone to, the claim is denied outright and it becomes a criminal matter. Insurance covers accidents and disasters, never deliberate destruction by the policyholder.

- Vacant or unoccupied homes. Many policies limit or exclude coverage once a home has sat vacant beyond a set period, often around 30 to 60 days. If you own a property that will be empty for a while, ask your agent about a vacancy endorsement, because a standard policy may not pay for a fire in a home no one is living in.

Outside of those situations, an accidental fire, the kind that makes up the overwhelming majority of house fires, is a classic covered claim. The exclusions exist to stop fraud and to account for the higher risk of an empty home, not to trap ordinary homeowners.

Why a Restoration Company Gets Involved

People often assume a fire is a job for a general contractor alone, but the first and most urgent phase after the fire is out is restoration, not reconstruction. Before anyone can rebuild, someone has to stabilize the property, extract the firefighting water, dry the structure, and clean the corrosive smoke and soot before it does permanent damage. That mitigation work is time-sensitive and specialized.

That is exactly where a fire restoration company fits. Our fire damage restoration crews handle that critical early stage: extracting the water, drying the structure to prevent mold, and cleaning the smoke and soot so it stops damaging your home and belongings. We also document the moisture readings and the extent of the damage, which is precisely the kind of evidence your insurer wants to see, so the mitigation and the claim move forward together instead of against each other.

✅ Mitigate First, and Keep the Records

Your policy expects you to take reasonable steps to prevent further damage after a fire, known as your duty to mitigate. Board up openings, extract standing water, and start drying and soot cleanup promptly rather than waiting weeks for every detail of the claim to settle. Document everything with photos and keep all receipts. A restoration company works alongside your adjuster, not against them.

Filing a Fire Damage Claim

Once your family is safe and the fire is out, a few steps in the right order make the claim smoother:

1. Make sure everyone is safe and the property is secure

Do not re-enter until the fire department says it is safe. Once you can, securing the property against weather and intruders, by boarding up windows or covering the roof, is both smart and part of your responsibility to prevent further loss.

2. Contact your insurer right away

Report the claim as soon as possible and get your claim number. Ask about your ALE coverage immediately if your home is unlivable, so you know where you can stay and what will be reimbursed.

3. Document everything before you clean or throw anything out

Photograph and video the damage thoroughly, and make a list of damaged and destroyed belongings. Do not discard damaged items until the adjuster has seen them or told you it is fine, because they are evidence of your loss.

4. Bring in a restoration company to mitigate the damage

Get professional mitigation started to stop the damage from getting worse. Water needs extracting, the structure needs drying, and soot needs cleaning before it sets in. For a deeper walk through the process, see our fire damage insurance claim guide. And if you rent rather than own, coverage works differently, which we cover in does renters insurance cover fire damage.