Yes, renters insurance covers fire damage, but only your side of it. An HO-4 policy replaces your personal belongings damaged by fire, smoke, and soot, pays loss of use costs while your unit is unlivable, and covers your personal liability if you accidentally caused the fire. It does not cover the building, which the landlord insures.

The Short Answer

Yes, renters insurance covers fire damage, but it is important to be clear about what it covers. A renters policy, often called an HO-4, is designed to protect you the tenant, not the building. It steps in for three things after a fire: the personal belongings you own that were damaged or destroyed, the extra living expenses you rack up when your unit is unlivable, and your personal liability if you were the one who accidentally started the fire.

What it will not do is rebuild the apartment or house itself. That structure belongs to your landlord, and their insurance covers the building. Your landlord's policy will do nothing to replace your furniture, clothes, or electronics, which is exactly the gap a renters policy is built to fill.

The Three Things Renters Insurance Covers

Almost everything a renters policy does after a fire falls into one of three buckets. Keep these straight and the rest of the process makes sense:

- Personal property. Your belongings, from the couch to your laptop to the clothes in the closet, damaged by fire, smoke, or soot.

- Loss of use. The added cost of living somewhere else, a hotel, meals out, and similar expenses, while your home is being repaired and you cannot stay in it.

- Personal liability. The costs you could be on the hook for if a fire you accidentally caused spread to a neighbor's unit or injured someone.

The one thing missing from that list is the building. That is the deliberate dividing line between a tenant's policy and a landlord's policy, and it is worth understanding before you ever need to use it.

💡 The Landlord's Policy Does Not Cover Your Stuff

This trips up a lot of renters. Your landlord almost certainly carries insurance on the building, but that policy exists to protect their property, not yours. If a fire destroys everything you own and you have no renters policy, the landlord's coverage will not replace a single item. Your belongings are your responsibility to insure.

Your Belongings: Personal Property Coverage

This is the heart of a renters policy. Personal property coverage pays to repair or replace the things you own that a fire damages, up to the limit you chose when you signed up. That includes furniture, electronics, appliances you brought in, kitchenware, clothing, and just about everything else that would fall out if you turned your apartment upside down.

Two details matter here. First, your coverage limit needs to actually reflect what your belongings are worth. People routinely underestimate this, then discover after a fire that their limit does not stretch to cover everything. Second, whether you have replacement cost coverage or actual cash value changes your payout. Replacement cost pays what it costs to buy the item new today. Actual cash value subtracts for age and wear, so an eight-year-old TV pays out far less. Check which one your policy uses before you need it.

Smoke and Soot Damage to Your Stuff

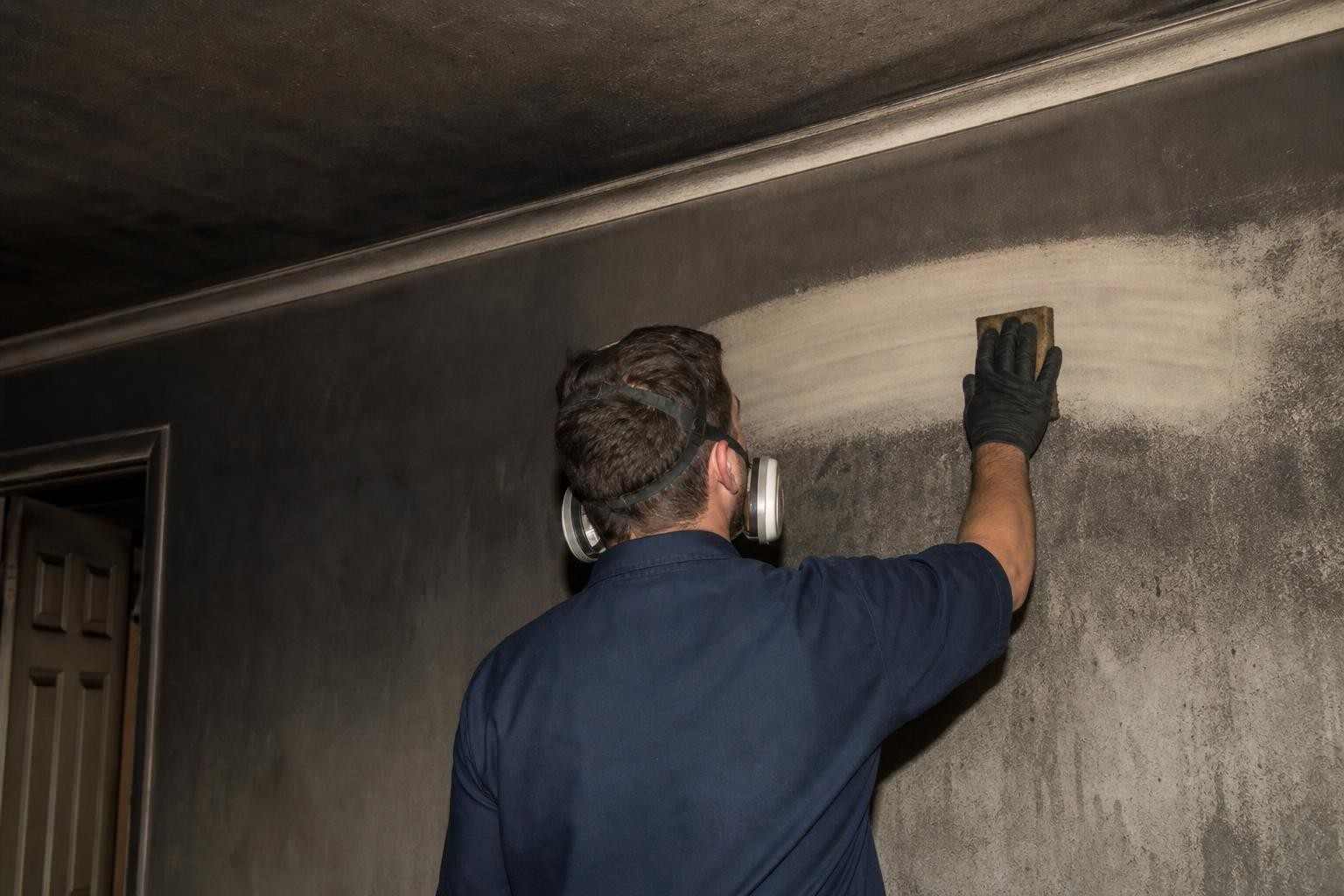

Fire rarely ruins only what it touches directly. Smoke and soot travel through a home and coat, stain, and saturate belongings in rooms the flames never reached. The good news is that a renters policy treats smoke and soot damage as part of the fire loss. If your clothes reek of smoke, your electronics are fouled with soot, or your furniture is stained, those items are generally covered right alongside anything that burned.

Soot is corrosive and smoke odor sinks deep, so professional cleaning often saves items that look like total losses at first glance. Our smoke and soot damage cleanup crews handle exactly this kind of work, and it pairs with full fire damage restoration when the unit itself took a hit. Do not throw damaged items out before they are documented, because that record is what supports your claim.

✅ Document Before You Toss Anything

Photograph and video everything the fire, smoke, or soot touched before you clean up or throw it away. Then build an itemized list of what was lost, with rough values and any receipts or photos you already had. This inventory is the single most useful thing you can do for a smooth, well-paid claim, and it is far easier to do now than to reconstruct from memory later.

Living Costs: Loss of Use

If a fire makes your rental unlivable, you still have to sleep somewhere and eat, and those costs add up fast. This is where loss of use coverage, sometimes labeled additional living expenses or ALE, comes in. It reimburses the reasonable extra costs of living away from home while your unit is repaired, above and beyond what you normally spend.

In practice that can mean a hotel or short-term rental, restaurant meals when you have no kitchen, extra fuel for a longer commute, and similar expenses. The key word is extra. Loss of use covers the difference between your normal cost of living and your higher cost while displaced, not your regular rent. Keep every receipt, because reimbursement is based on documented spending, and there are usually limits on the total and the time period.

If the Fire Was Your Fault: Liability

Here is a scenario renters do not think about until it happens: you leave a candle burning or a pan on the stove, a fire starts, and it spreads to the units next door. Now the damage is not just yours. This is what personal liability coverage is for. If you accidentally cause a fire that damages other people's property or injures someone, your renters policy can help cover those costs and defend you if you are held responsible.

It is worth being precise: liability applies to accidents, not to fires you set on purpose. And it protects other people's property and injuries, not your own belongings, which fall under personal property coverage instead. For a tenant, this piece is quietly one of the most valuable parts of the whole policy, because the cost of a fire spreading through a building can dwarf the value of your own things.

⚠️ Arson and Neglect Are Excluded

Insurance covers accidents, not intent. A fire you deliberately set is never covered, and neither is the liability for it. Coverage can also be challenged if the loss came from serious neglect. As with any policy, the protection is built around fires that happen to you, not fires you cause on purpose.

What Renters Insurance Does Not Cover

Knowing the edges of the policy is as important as knowing what is inside it. A standard renters policy generally will not cover:

- The building structure. Walls, floors, the roof, and built-in fixtures belong to the landlord and are covered by their policy, not yours.

- Your roommate's belongings, unless they are named on your policy. Each person usually needs their own coverage.

- Fire from a flood. Flooding is excluded from renters policies and needs separate flood coverage, though that is a different peril than fire.

- Intentional fires. Arson by the policyholder is never covered.

- Amounts above your limits. Losses beyond your chosen personal property or loss of use limits come out of your pocket.

The recurring theme is the line between the tenant and the building. If it is the physical structure, it is the landlord's. If it is your belongings, your living costs, or your liability, it is yours to insure, and a renters policy is what does it.

How to File a Renters Fire Claim

Once everyone is safe and the fire is out, moving through the claim in the right order keeps things smooth:

1. Make sure everyone is safe first

People before property, always. Do not re-enter a fire-damaged unit until the fire department clears it, and be cautious of structural damage, lingering smoke, and electrical hazards.

2. Report the claim promptly

Call your insurer as soon as you reasonably can and open the claim. Get your claim number and ask what documentation they need. Reporting promptly is part of your responsibility as a policyholder and keeps the process from stalling.

3. Document and itemize your belongings

Photograph and video the damage, then build an itemized inventory of what was lost, with descriptions, rough values, and any receipts or old photos you can find. Do not discard damaged items until they have been documented and your insurer says it is fine to do so.

4. Save your living-expense receipts

If you are staying in a hotel or eating out because your unit is unlivable, keep every receipt. Loss of use reimbursement is based on documented extra spending, so a shoebox of receipts turns into real money back.

5. Get professional cleanup started

Bring in a restoration company to handle smoke, soot, and fire residue on the things that can be saved. Our fire damage restoration team responds around the clock and can document the damage in a way that supports your claim. For the coverage side of a fire loss, our guide on whether homeowners insurance covers fire damage covers the property-owner angle, and our fire damage insurance claim guide walks the full claim step by step.