To file a fire damage insurance claim, confirm the property is safe to re-enter, contact your insurer promptly for a claim number, then document every room with photos, video, and a written inventory before you clean or discard anything. Secure the property, keep all receipts including temporary housing, get a restoration estimate, and claim the smoke, soot, and firefighting water too.

What a Fire Claim Actually Covers

Fire is one of the core perils that a standard homeowners policy is built to cover, which is good news on a very bad day. A typical policy pays to repair or rebuild the dwelling structure, replaces your personal property up to your limits, and covers the damage that comes with the fire even when the flames never touched it. That last part surprises people, so it is worth saying plainly: your claim usually includes the smoke and soot that spread through the house and the water damage from the firefighting effort, not just the burned area.

There are limits. Coverage applies to the fire itself and its direct consequences, and arson by the homeowner is excluded for obvious reasons. But for an accidental house fire, kitchen fire, electrical fire, or wildfire, the structure, your belongings, the smoke and soot, the firefighting water, and temporary housing are all typically on the table. Knowing that up front stops you from under-claiming. If you want the coverage basics first, start with our guides on whether homeowners insurance covers fire damage and, for tenants, whether renters insurance covers fire damage.

💡 The Damage You Cannot See Is Still Covered

Smoke and soot travel into wall cavities, HVAC ducts, and soft materials far beyond the room that burned, and the water used to put the fire out soaks floors and ceilings below. All of it is part of a standard fire claim. If you only document the charred spot and ignore the rest, you leave real money unclaimed.

Filing Your Claim, Step by Step

The order matters. Do these in sequence and the whole claim goes smoother.

1. Make sure it is safe, and that you are cleared to go back in

A fire-damaged home can be structurally unsound, full of toxic smoke residue, and carrying live electrical or gas hazards. Do not re-enter until the fire department or another authority has cleared the property. Your safety comes before any photo or phone call.

2. Contact your insurer promptly and get a claim number

Report the loss to your insurance company as soon as you reasonably can, and write down the claim number they give you. That number is the thread every later conversation hangs on. Reporting promptly also protects you, because delay is one of the things insurers can push back on.

3. Document everything before you touch it

This is the step that pays for itself. Photograph and video every room, every damaged surface, and the contents, before you move or clean anything. Then build a written inventory of what was damaged or destroyed, item by item, with rough age and value where you can. The more complete your record, the harder it is for anyone to shortchange the claim.

4. Secure the property so it does not get worse

Your policy expects you to take reasonable steps to prevent further damage, which is called your duty to mitigate. That usually means a board-up of broken windows and doors and a roof tarp if the roof was breached, so rain, weather, and trespassers cannot add to the loss. Keep the receipts for this work, because it is part of the claim.

5. Keep every receipt, including temporary housing

Save receipts for everything you spend because of the fire: emergency lodging, meals, board-up work, essential replacements. Many of these fall under Additional Living Expenses, covered below, and you can only be reimbursed for what you can prove.

6. Get a professional restoration estimate

An independent estimate from a restoration company gives you a real number for what it will take to make the home whole, and something to compare against the adjuster's figure. Our fire damage restoration team documents the full scope, from structural damage to smoke and water, so nothing gets missed.

7. Work with the adjuster

The insurer sends an adjuster to inspect the loss and price the claim. Walk them through your documentation, hand over your inventory, and make sure the smoke, soot, and firefighting-water damage are all in their scope. More on this below.

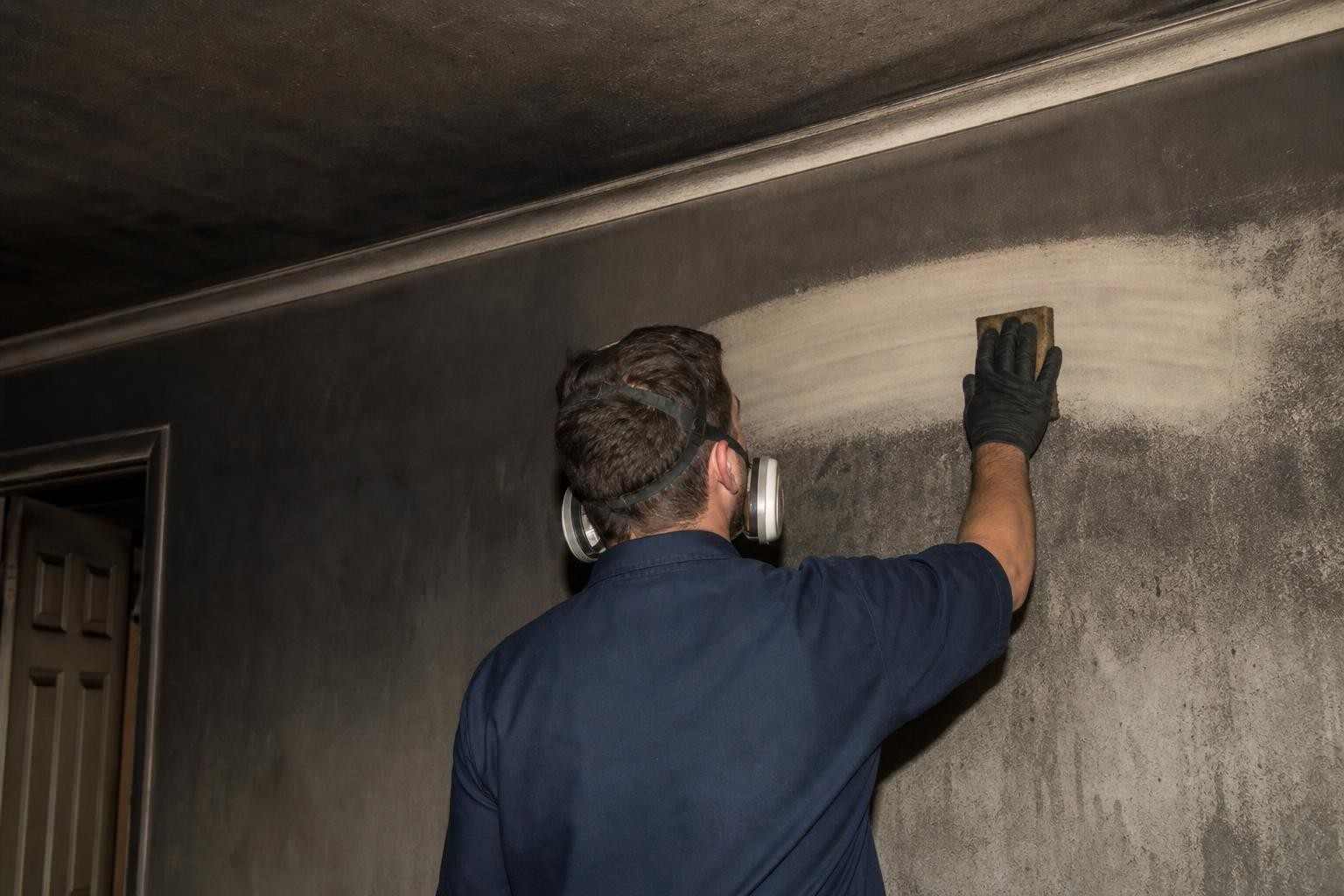

Do Not Forget the Smoke and Water Damage

The fire itself is only one of three problems, and the other two are easy to under-claim. Smoke and soot coat surfaces well beyond the burn area, seep into porous materials, and leave an odor that ordinary cleaning will not remove. Professional smoke and soot damage cleanup is often a bigger part of the claim than the fire damage itself, especially in a smaller fire that filled the whole house with smoke.

Then there is the water. Putting out a fire dumps a large volume of water into the structure, and that water behaves like any other water loss: it soaks into floors, drywall, and ceilings, and it can start growing mold within a day or two if it is not extracted and dried. Getting water extraction started quickly protects both your home and your claim. Make sure both the smoke damage and the firefighting water are written into your loss, not just the flames.

⚠️ Three Losses, One Fire

Fire, smoke and soot, and firefighting water are three separate types of damage from a single event, and all three are typically covered. Claim only the visible fire damage and you may miss the majority of the loss. Document each one on its own.

Additional Living Expenses: The Benefit People Miss

If the fire makes your home unlivable, your policy almost certainly includes Additional Living Expenses, usually shortened to ALE and sometimes called loss of use. This coverage reimburses the extra costs of living somewhere else while your home is repaired: a hotel or rental, meals above what you would normally spend, and other reasonable added expenses of being displaced.

ALE is one of the most commonly overlooked benefits in a fire claim, because in the chaos right after a fire people focus on the house and forget the coverage that helps them live in the meantime. Start saving lodging and expense receipts from day one, and ask your insurer specifically about your ALE limit when you open the claim.

✅ Keep a Simple Expense Log

From the first night, jot down every fire-related expense and keep the receipt: lodging, meals, laundry, essential replacements, travel. A running log makes your ALE claim easy to submit and hard to dispute, and it means you are not trying to reconstruct weeks of spending from memory later.

Common Mistakes That Cost You Money

Most of the money lost on a fire claim is lost in the first few days, through a few avoidable mistakes:

- Throwing things out before documenting them. Damaged items are evidence of your loss. Once they are in a dumpster, they are hard to claim. Photograph and inventory everything first, even the things you are certain are ruined.

- Over-cleaning before the adjuster sees the damage. Scrubbing away soot and hauling out debris before the inspection erases proof of the loss. Document the full extent first, then mitigate. There is a difference between securing the property and erasing the evidence.

- Missing the ALE benefit. Not tracking temporary housing and living costs, or not knowing the coverage exists, leaves money on the table that your policy already promised you.

- Under-claiming the smoke and water. Focusing only on the burned area and ignoring smoke, soot, and firefighting water is the single most expensive oversight.

- Waiting too long to report. Delay gives an insurer a reason to question the claim. Report promptly, even while you are still shaken.

Working With the Adjuster

The adjuster works for the insurance company, and their job is to assess and price your loss. That does not make them the enemy, but it does mean you should come prepared. Have your documentation and written inventory ready, walk them through every affected area including the ones that only have smoke or water damage, and give them your independent restoration estimate to compare against.

If your numbers and theirs are far apart, you are allowed to ask questions and provide more evidence, and for a large or complicated loss some homeowners bring in a licensed public adjuster who works for them rather than the insurer. A good restoration company is used to working alongside adjusters and can document the moisture readings, smoke spread, and structural scope that support a fair settlement. Our Dallas fire and smoke restoration crews do exactly that.

How Long a Fire Claim Takes

There is no single answer, because it depends on the size of the loss and how complete your documentation is. A small, well-documented fire claim can move in a matter of weeks. A major structural loss with rebuilding, contents replacement, and ALE can run for months. The two things most in your control are speed and paperwork: reporting promptly, documenting thoroughly, and responding quickly to the insurer's requests all shorten the timeline.

Getting cleanup and drying started early helps here too. The sooner the smoke residue and firefighting water are dealt with, the less secondary damage piles up while the claim is being processed, and the clearer the final scope becomes. If your fire also left standing water, our emergency water removal team can respond around the clock so the water does not turn into a mold problem on top of everything else.